As a marketer, you might have seen reference to CLV, or customer lifetime value. Sometimes referred to as lifetime customer value (LCV), this is a useful metric that can be handy when managing your marketing budget or strategy.

By understanding how much a customer may spend with your company over a period of time, you can work out your optimum cost per acquisition (CPA) for one customer. This in turn will inform things like how much you spend on paid advertising, and how much to put into other marketing channels such as your content marketing, email or whatever else you need to pay out.

Before we look at how to work out CLV, we’ll look at exactly…

What is Customer Lifetime Value (CLV)?

CLV is an estimation of the potential revenue earned from a single customer account. You’re best to work out the total value net, and then do the deductions later to work out the gross. The timescale for ‘lifetime’ will be a sliding scale based on a number of factors such as your product, the service you offer and the cost of your service.

For example, someone buying a new car from a showroom may then come back for parts and maintenance over the duration of their car ownership. That might be five or ten years, or it might be until the warranty runs out and they decide to use a local (cheaper) mechanic.

A casual shopper looking for clothes might use an ecommerce website twice a year, perhaps in line with the seasons or sales cycles. Or someone might buy your coffee and cakes three or four times a week on their way to work.

But, someone looking for financial advice around starting a business might need ongoing financial products and services for many years.

To calculate the formula for customer lifetime value, you’ll first need to understand your customer lifetime cycle.

Understanding Your Customer Lifetime Cycle

We already mentioned that your product and service will be a factor in your customer lifetime cycle. But, for some businesses, there may be no definite end to a customer lifecycle. People may buy from you again a year or two after their first interaction, or they may use your subscription service indefinitely.

In these instances, you can always work with a specific period of time, such as one year or five years, to help understand what you might expect to see back from winning one customer.

To do this, take a look at your customer account activity in your CRM to get an idea of how long your customer lifetime is. If you’re dealing with thousands of clients, it might be worth picking a cross section of them to give you an idea.

For some, this won’t be possible due to the nature of your business, perhaps if you don’t use a CRM to monitor your client activity. Your bricks and mortar hardware store might not make a note of the same old guy who has been coming in every week for 30 years spending who knows how much…

You can still work out your CLV without having a database of client purchases, but you’ll need to use a slightly different method, which we’ll come to shortly.

OK, so what about understanding the actual value of a customer’s activity?

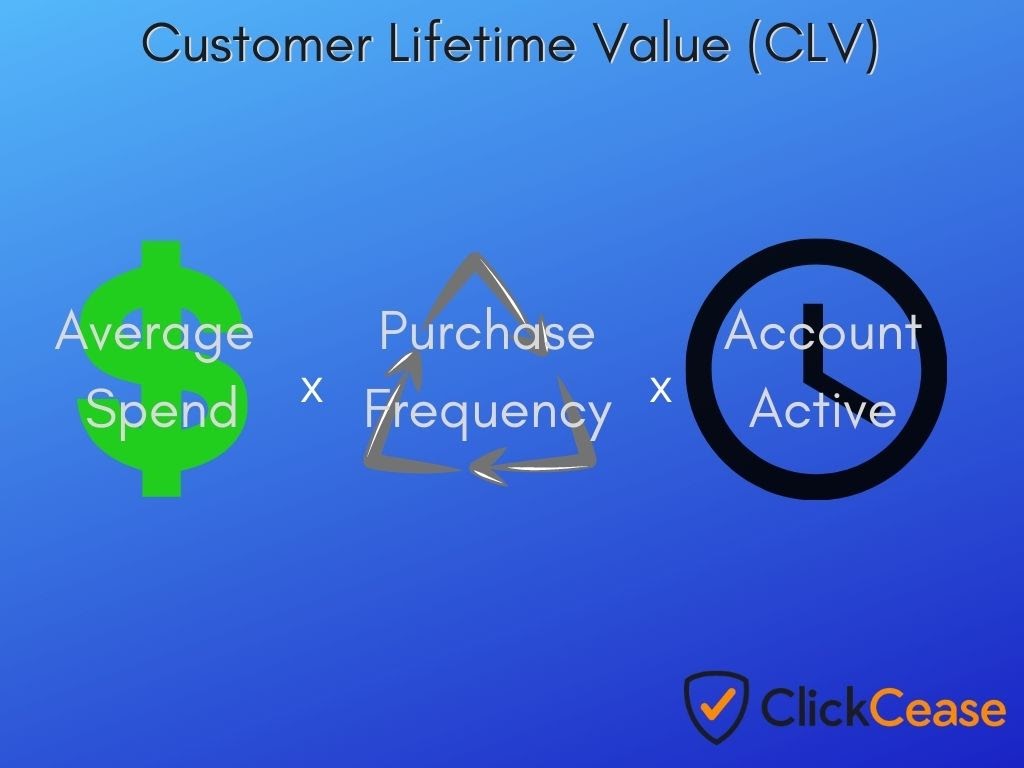

How to Calculate CLV

The formula to calculate your customer lifetime value will look something like this.

(Average purchase value x Average purchase frequency) x average length of customer account activity

So, let’s use a toyshop as an example. Let’s say you have two kids. That’s two birthdays and Christmas (or whatever cultural celebration you want).

If you spend approximately $100 per child, per celebration, you’re looking at four purchases in a year – and let’s say you use the same toy shop every year until your kids are 16.

($100 x 4 = $400) x 16 years = $6,400

Another example: You offer a premium automation package for digital marketing agencies at $99 per month, which the average account uses for 3 years.

($99 x 12 = $1188) x 3 years = $3,564

Of course, these are just guideline figures. But, you can see how that can apply to your business too.

Working out the CLV without a database

You’re not using Salesforce, Sage or any other CRM to track your customer spend? Perhaps you have a food business or other service that doesn’t require logging client details. How can you work out your average customer lifetime value?

Never fear. These steps can help you formulate your lifetime customer spend, although some of this might require estimations and some research of your own.

1. Average purchase price

Work out your average purchase price. You can do this based on a daily or weekly average if it helps to simplify things.

The formula for average purchase value is:

Total revenue (daily, weekly or whatever) / Purchase volume (assuming that one customer makes one purchase)

Example: $22,000 / 500 purchases = $44

2. Purchase frequency

Next up, you’ll want to know how often your customers buy from you. You could either select a decent sample size of customers and ask them directly how often they use your business. Or, you could do a visual survey of your visitors to your location – making a note of repeat customers on different days.

Visit frequency x average purchase cost

Example: 4 weekly visits x $5 = $20 per week

3. Service usage lifetime

Now, understanding how long they use your service for is another matter. Again, it may come down to chatting to your clientele. Do they visit your business every week, every month, a couple of times a year?

With a good enough sample size, you can build a decent picture of your average customer lifetime cycle, and in turn get that CLV figure.

(Average spend x average visit volume) x lifetime cycle duration

($44 per spend x 3 times a year = $132) x 5 years = $660

Whatever your business model or your product, you can adapt the formula for customer lifetime value to help make your marketing a bit more effective.

What can you do with CLV?

So, you know that your average customer will spend $1000 net in a year with you. You can then work out your gross deductions and get a good idea of how much you’re actually making from that one account.

Based on that, how much would you be prepared to win one new customer?

This is known as the target CPA (cost per acquisition) and is a metric used by search marketing platforms like Google and Microsoft for PPC ads.

Having the insight into your average and target CPA can be invaluable when it comes to creating a marketing strategy. Of course, this can inform how much you’ll be willing to spend on specific platforms, and even help you work out which marketing strategies are most cost effective.

Understanding the lifetime value of a customer can also help you with that sales funnel, and building retargeting campaigns to keep people coming back. After all, keeping customers brand loyal and even turning them into advocates for your brand is much more time and cost effective than pitching for new custom all the time.

Maximising the Customer Lifecycle

Your customer lifetime cycle actually begins before they make a purchase. You already know about sales funnels (you do, right?), and how top of the funnel (ToFu) is where you get their attention, middle of funnel (MoFu) is where you win their trust and bottom of funnel (BoFu) is where you make the sale.

In terms of actual lifetime value, you’re obviously going to be working out how much your average customer spends, which is BoFu. But, the rest of the funnel is also just as important for keeping customers in your cycle and ensuring you maximise that lifetime value.

Customer retention is a combination of great support and customer service, regular content that addresses your target audience’s pain points, effective retargeting and, obviously, a great product.

Whatever channels you’re using to reach your customers, and to keep them coming back, understanding the customer behaviour throughout their journey with you is key to extending their lifetime value with you.

Getting value for money from programmatic ads

Pay per click has become the go to advertising method for most businesses online. And, there is a lot of choice from Google and Facebook to platforms like RevContent and Taboola.

Although programmatic ads are incredibly useful, and can be very effective, getting your ROAS from them is a job in itself. If you’re managing your own marketing in house, or if you’re an agency or PPC manager, you’ll already know there are a lot of metrics to keep an eye on to increase your return on investment.

One key step is to prevent invalid clicks on your ads, which can be both costly and damaging to your marketing campaign. These are non-genuine clicks on your paid ads, often from automated sources such as bots, but can also be from malicious actors like business rivals or brand haters.

ClickCease is the industry leading click fraud prevention software, covering your paid ads on Google Ads and display network, YouTube, Facebook Ads and Microsoft/Bing Advertising. If you want to be assured that your ads are only being seen by real potential customers, check out ClickCease for free.

Is it worth using ClickCease? Check out what our customers have to say (external link)